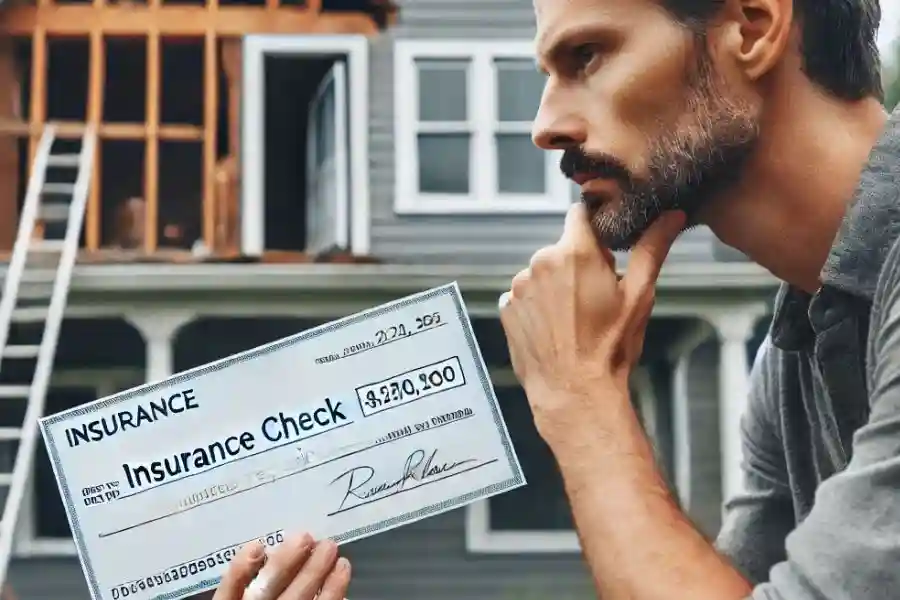

If you file a lawsuit and the insurance company misses you a check, many people assume that money is especially dedicated to cover the damaged parcel. But what if you do not spend insurance money on repairs?

Whether it be home, auto, or another property-related insurance, many people begin to question whether they are required to use the funds exclusively on repairs or if they can take that money and spend it elsewhere. This article will cover the ramifications of not fixing anything with insurance payouts, your options instead, and some legal information.

Key Takeaways:

- Insurance payouts are generally intended for repair purposes, but some flexibility may exist.

- Misusing the money can lead to contractual violations with your insurer or penalties from mortgage lenders.

- Alternatives exist, but careful consideration is needed to avoid negative consequences.

- Homeowners and car owners often face different regulations when it comes to how insurance payouts are used.

Understanding How Insurance Payouts Work

If a declaration is made and the insurance business supports the payment, you’ll obtain either a check or an immediate promise to cover the damages cited in your claim. However, if the injury isn’t close, many are surprised if they can keep the cash or use it for other goals, like spending off their mortgage.

Homeowner’s Insurance covers financial threats from effects of damage and other insured happenings, like natural catastrophes. Auto Insurance covers car damages from accidents or non-collision happenings like theft or destruction. Renter’s Insurance mainly covers personal belongings, not the rental form.

- Free Money Fallacy: It might seem like insurance payouts are free money, but there are terms and responsibilities. Ignoring them can lead to serious consequences.

- Statistical Insight: In the U.S., homeowner’s insurance claims averaged $12,785, showing the significant responsibility attached to these payouts.

Legal and Contractual Obligations of Using Insurance Money for Repairs

The first thing to think about is what obligations come with receiving the insurance payout, legally and contractually. Something many people do not realize is that, if there are other parties also involved in this process, such as a mortgage lender or leaseholder, you will probably be contractually obligated to use the money for repairs.

Involvement Of Mortgage Company

If you have a mortgage, the lender may be named as a co-payee on your insurance check. How the funds are used is, after all, an interest of their own. Lenders usually insist that this money only goes toward repairs, so the property remains valuable if they need to seize it as collateral against your mortgage.

Similarly, if you have a lienholder on your vehicle or are a leaseholder, they may tell you how auto insurance payouts can be used. Using the money for anything but repairs could violate the agreement you signed when securing that loan or lease.

Expert Opinion: “It is not unusual for a lender to decline insurance claim funds due if they are neglected in the process of resolving an insurance event.”

Potential Legal Consequences

- Policy cancellation: Your insurance provider can cancel your policy if they learn you’re not using the money to pay for the necessary repairs.

- Lender Penalties: Mortgage companies or lienholders may charge you penalties or increase your interest rates.

- Litigation: In the event of serious misuse, insurers or lenders may seek recourse through litigation.

The Financial Risks of Not Using Insurance Money for Repairs

Some might want to keep the money, but long-term financial risk far outweighs the immediate reward. This part examines what happens in the long run as a result of not fixing things.

- Lower Property Value If you fail to do the repairs with homeowner insurance cash, this can decrease your house value drastically and pose a problem when selling or refinancing.

- A Delay in Repair Increases Price Damages may become worse if put off, costing you more than the original repair amount. For example, a small roof leak can lead to a major structural issue if left unattended.

- Future Insurance Claims Denied If you are paid for repairs but don’t address the damage, future claims may be denied for related issues. Insurance companies can refuse coverage for problems arising from not fixing the initial damage.

Tip: It’s always wise to get multiple quotes from contractors to ensure your insurance payout covers the costs. Some companies may be willing to negotiate if the payout falls short.

Alternatives to Using Insurance Money for Repairs

While insurance payouts are meant to be used for repairs, there may be circumstances where you don’t want or need the repairs done right away. Here are some alternatives people often consider:

Keeping the Money

In some cases, you can keep the payout. This is more common with auto insurance, as fewer stakeholders (like mortgage companies) are involved. However, it’s crucial to recognize that by doing this, you’re taking a considerable risk.

Using the Money for Other Expenses

You might decide the repair isn’t urgent and use the insurance money for other expenses. For example, homeowners may prioritize paying off debt or tackling a different home improvement project. While this can seem practical in the short term, it may lead to complications if the original damage worsens.

Should You Repair or Reinvest? Making the Right Decision

On other occasions, the choice of spending insurance money on its intended purpose isn’t so clear-cut. Here’s a framework to figure out what’s best for you:

Determine the Extent of Damage

Is the damage serious enough to require immediate attention? For minor issues like a small scratch on your car or cosmetic damage at home, delaying repairs might not have significant consequences.

Future Financial Impact

Will making repairs today affect your property or vehicle’s long-term value? For homeowners, neglecting to fix a roof or siding can lead to even more costly repairs down the road. For car owners, not repairing a vehicle could significantly reduce its resale value.

Speak to Experts

Before making a final decision, consult an insurance agent or legal expert. They can clarify your contractual obligations and help you understand the potential consequences of diverting funds. Ideally, get written confirmation from your insurance company or lender before using the money for anything other than repairs.

Mortgage and Lender Requirements for Home Insurance Payouts

Again, your mortgage lender will be highly concerned with where insurance payouts are going. Here’s a more detailed look:

Escrow Accounts for Large Payouts

If the damage is significant, like from a natural disaster, the lender may control the insurance payout by depositing it into an escrow account. These funds are released only when specific repair milestones are met to ensure the money is used for repairs.

Lender Inspections

For larger claims, most mortgage lenders require post-repair inspections to verify that the insurance money was spent correctly. Failing these inspections can lead to legal and financial issues.

Know How Your Mortgage Is Contracted

The terms of your mortgage contract will dictate how insurance payments are processed. Be sure to read these carefully or contact your lender to fully understand your obligations.

The Role of Contractors and How They Affect Insurance Payouts

Hiring a contractor will impact the insurance payout process. Working with licensed and insured professionals ensures the job meets standards and adheres to your insurance company’s guidelines.

- Working with a Contractor When hiring a contractor, choose one with experience in handling insurance claim work. Ask for detailed quotes and deadlines. Some insurance companies may require pre-approval of contractors or proof of licensed work before releasing the full payment.

- Post-Maintenance Documentation Keep all bills, receipts, and communication with the contractor. Insurance companies may need this documentation to close out the claim.

Tip: Before starting repairs, get your contractor’s opinion on the sufficiency of the payout. In some cases, contractors may identify additional damages that need to be accounted for, allowing you to seek further compensation.

Conclusion

All in all, deciding what happens if you do not use insurance funds for repairs is no clear decision. How you use your insurance payout can have severe financial, legal, and contractual importance. Whether you are filing a home or auto insurance claim, understanding what’s needed of you and the risks concerned will help you make an educated conclusion about your situation.

Were you ever in a position where you had to decide whether to use your insurance money for something else rather than repairs? What were the results, and what did you learn? Share your adventures and check out more of our articles for top tips on managing insurance claims.